Thank you to all the families for being the greatest clients!

Check out our latest video of our recent client event at Kustermans.

Thank you to all the families for being the greatest clients!

Check out our latest video of our recent client event at Kustermans.

If you blinked you would have missed it. The housing market was on fire in February with houses on the mls (multiple listing service) seeing record price increases.

Home buyers were lined up down the street to get a showing. Open houses were bursting at the seams. It was not uncommon to receive 30 offers on a house and have it sell for thousands of dollars above the asking price.

There simply was not enough housing supply to keep up with the buyer demand. This led to an unprecedented market. It was a terrible situation for buyers to try and buy a home and absolute calamity for most home sellers, unless you moved to a hotel—which some sellers did. A crazy environment for buyers and sellers.

Today it’s the polar opposite. Selling your home is no longer quick. Some home sellers are begging for an offer. Others struggle to even get showings.

Home equity is dwindling compared to purchase prices of February. It is literally the opposite of February’s market. Certain sellers are panicking because they bought a house banking on the proceeds from their sale.

So, what’s in store for the market? I’ll liken it to a Saturday afternoon cruise down Highway 401. Your speedometer says 160 km/h. You’re driving a Lamborghini and there are no speed traps in sight.

Then, off in the distance, there are red lights. Traffic is building and, all of a sudden, you’re forced to reduce your speed because you’ve come upon a traffic jam.

The traffic jam represents buyer fatigue, astronomical seller price expectations and rising interest rates. Like a traffic jam, these factors cause the market to slow down.

The Central Bank of Canada made it clear they would raise interest rates in the short term affecting monthly mortgage payments (monthly payments) on fixed rate mortgages and variable rate mortgage payments. A recent update by Connolly Capital Mortgage Solutions, a leading Canadian mortgage brokerage, shows Canada’s 5-year government bond has been volatile as of late, but has consistently remained under 3% for the last three months.

Investors and banks are pricing for inflation risk, so they are continuing to raise fixed rates. Conventional fixed rates are well over 4.50% now and alternative lending deals are over 5.00%.

Why does this all matter? It matters because it affects interest rates and iterate rates affect a buyer’s ability to borrow money. The higher the interest rate the higher the cost to borrow. Other factors like the consumer price index (CPI) and inflation (rising costs of goods and services) will affect a buyer’s ability to get a mortgage loan.

The consensus appears to indicate another 0.50% hike to the Bank of Canada’s Prime Lending Rate. This would bring the Prime to 3.70%. Ultimately, the Bank of Canada is slowing growth by raising rates, which is affecting purchase prices amongst housing and other goods and services. Home buyers will continue to shop banks and alternative lenders for the lowest rate.

Most home buyers will ultimately have to decide whether to go with a fixed rate mortgage or a variable rate mortgage. It’s recommended to speak to a mortgage broker (or mortgage brokerage) or your financial institution and build a plan based on potential annual percentage rate (APR) increases or decreases. They may have to increase the amortization period to bring down monthly payments.

They can help determine monthly mortgage payments based on a home’s equity. This can help save you thousands of dollars just by strategizing. It’s also beneficial to know what your regular payments will be.

So, what’s in store for the remainder of the year? Where did all the pent-up demand from buyers go that was so abundant in the first quarter? Don’t be surprised if the market does normalize.

Buyers will be used to higher interest rates. Sellers’ expectations will have adjusted and people need homes for growing families, downsizing, readjusting capital, investment and for many other reasons. Don’t be surprised if the market picks up steam towards the end of the year—albeit, perhaps, not at the rate we saw in February.

Immigration continues to be a big factor when it comes to forecasting the housing market. With north of 400,000 immigrants coming to the country a year, this creates demand. And demand affects housing prices. The real estate market is driven by supply and demand. Mortgage rates will affect rising house prices in the interim with mortgage payments increasing. Real estate agents know all to well that dips in the market do happen. Inflation prices across the board are being curbed by the bank of Canada to slow prices. Especially for Toronto house prices, one could argue we need a break pedal.

Mississauga real estate prices have dropped on a detached home for the first time in a long time but there continues to be demand. The same goes for Oakville housing prices, Burlington and Hamilton Housing prices. With new immigrants wanting to live in the GTA, it’ll be interesting to see where there tipping point of supply and demand plays out.

Tertiary markets like London continue to be a hot bed for investors and young families looking for more affordable housing. London home prices have dropped marginally but continue to do well because of higher demand.

The Burlington housing market should be quick to rebound given its proximity to the city of Toronto and family favorable neighbourhoods.

For a further discussion as it pertains to your situation or to gain further insight, please reach out to The Regan Team at info@reganteam.ca

Don’t look now, but what has happened to the real estate market? Only weeks ago, it was pandemonium for buyers trying to lock in a home purchase before the seasonally adjusted craziness of the spring market. Bidding wars saw dozens of offers. Homeowners vacated to hotels in preparation for the frenzy of buyers that would soon be lining up down the street for showings. The winds, however, have shifted and now sellers are starving to get an offer, let alone a showing.

The market has changed for a variety of reasons including buyer fatigue, rising interest rates and an increase in the housing supply.

At the beginning of the year, the Bank of Canada (BoC) announced that interest rates would rise in 2022. For the first time in over 20 years, the Bank of Canada increased rates by more than 0.25%, with a 0.50% hike to the Prime Rate. Prime is now 3.20%. The 50-basis-point hike shows that the bank understands it has fallen behind the curve in terms of fighting inflation and is now trying to catch up. This is slowing the growth of the housing market.

According to Matthew O’Neil of Connolly Capital Mortgage Solutions, one of Canada’s top mortgage brokerages, Canada’s five-year government bond is at a three-year high and will continue to increase. Investors are pricing for inflation risk and fixed rates continue to rise with five-year terms, now above 4% on conventional mortgages. This is putting pressure on buyers and challenging affordability.

Rising interest rates have put more stress on buyers who face fatigue in the market from the whirlwinds they faced in February. Many are missing out on the home of their dreams as a result of astronomical prices. Some houses are selling in a matter of hours, before a buyer even has a chance to see the home, causing even the most fit buyers to feel fatigued.

The good news for buyers in most markets across South-and Southwestern-Ontario is that we are seeing the usual spring flood of new inventory, which helps balance the supply and demand. Buyers who were pre-approved for a lower rate are hurrying to secure a purchase before their rate lock expires.

So what does this mean for sellers? I’ll gaze into the crystal ball and say that prices might stabilize instead of rising at unprecedented levels. Sellers will need to monitor supply in their given neighbourhood and watch the ebbs and flows of buyer demand. Interest rate hikes won’t help buyers or sellers but a lack of housing might offset the rise in rates and make for a more balanced market as we head into the second half of the year.

Interest rates and real estate go together like mashed potatoes and gravy. As a long-time barometer of housing prices, interest rates are a key indicator of determining whether housing prices will go up or down.

Simply put, if rates go down, the cost to borrow money in the form of a mortgage goes down, which increases the amount of people wanting to buy real estate—and demand. When rates go up, the opposite is true.

The Bank of Canada (BoC) will begin with an initial 25bp increase in policy rates in March, from 0.25% currently, with projected further hikes to end 2022 at 1.25% and 2023 at 1.75%. So, what does this actually mean? If the BoC increases or decreases its overnight interest rate, it does not necessarily mean the banks, where you and I go to get a mortgage, will follow suit. Remember, banks are businesses and they will compete for our business by offering the best rate they can.

According to Matthew O’Neil of Connolly Capital Mortgage Solutions, one of Canada’s top mortgage brokerages, as of writing this, a 5-year fixed comes in at 3.49% and a variable rate Prime of 0.80%, which equals a rate of 1.90%.

“The bottom line is the cost to borrow money is still historically low,” says O’Neil. “Which should continue to fuel buyer demand for the remainder of 2022.” Insert interest rate graph

Other key barometers to watch as they relate to housing prices are trends in immigration and population. According to StatsCan, Ontario’s population is projected to reach between 14,848,500 (scenario L) and 18,256,100 (scenario H) by 2038, that’s an increase from 13,538,000 in 2013.[1]

The three primary areas of residence for immigrants would remain Toronto (between 33.6% and 39.1%), Montréal (between 13.9% and 14.6%) and Vancouver (between 12.4% and 13.1%).[2] Population growth is good. As a country, we need it. But we have a problem. There are not enough homes for everyone to live in. Among the G7, Canada has the lowest average housing supply per capita, with 424 units per 1,000 people.[3]

At the rate we’re going, Canada, overall, would need 1.8 million more dwellings to have the same number of homes per capita as the rest of the G7.[4] Unless you believe in miracles, the housing shortage we are currently experiencing won’t be fixed anytime soon. Government bureaucracy at the provincial and municipal level combined with rising material and land costs don’t make it easy for developers to build.

Historically, we could watch what interest rates do to predict housing prices. In the past it was the key indicator to watch. Today, with what appears to be a prolonged historically low interest rate environment, the key barometers will be immigration, population growth and the scarce housing supply. If this continues, how high will housing prices go?

[1] StatsCan – Results at the provincial and territorial levels, 2013 to 2038

[2] StatsCan

[3] Financial Post

[4] Financial Post

When the pandemic hit in early 2020, the real estate market came to a screeching halt. Buyer showings were non-existent and For Sale signs loomed on lawns like a tumbleweed blowing down a deserted street in a scene from an old Western. If you were one of the many (including myself) willing to bet that this would drive down real estate prices, you would have been wrong. Based on data from the UBS Global Real Estate Bubble Index, from mid-2020 to mid-2021, real house-price growth in major cities around the world hit an increase of 6%, at the time the highest level since 2014.

In cities like Vancouver and Stockholm, prices jumped by double digits. The UBS study illustrates how much the cost of buying a modest apartment has changed over the past 10 years in 25 cities. Though Hong Kong has the highest average cost per apartment, Frankfurt and Toronto rank even higher for “bubble risk,” according to UBS, which based their findings on decoupling from local incomes and rents.

It’s no secret that real estate values are far outpacing the growth of family income. The argument that GTA housing is in a bubble has been whispered over the past 20 years. And yet, here we are, with a few ups and downs over the years but mainly ups. Low interest rates continue to fuel the housing demand and a shortage of inventory is creating a competitive buyer landscape like no other. The best recent example to offer is a property that received 45 offers and hosted 170 showings before selling for an unprecedented price.

So, are we in the making of a real estate bubble? Perhaps. Immigration will be an important factor to watch in 2022 and in the following years. More and more people want to live in our country and they are going to need a place to live. Are you ready to place your bet?

Source: Fortune December 2021/January 2022

UBS Global Real Estate Bubble Index

The following are the fourth quarter highlights condensed from the Royal LePage House Price Survey:

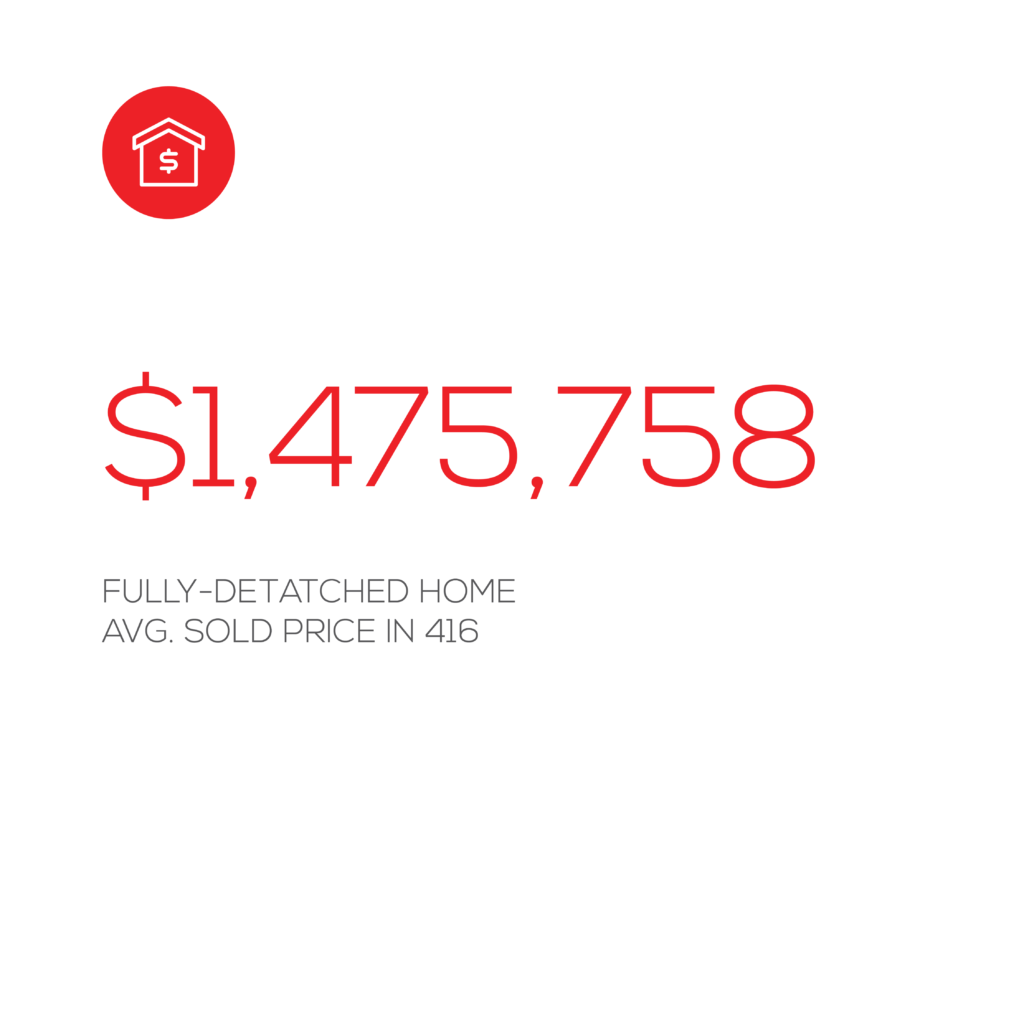

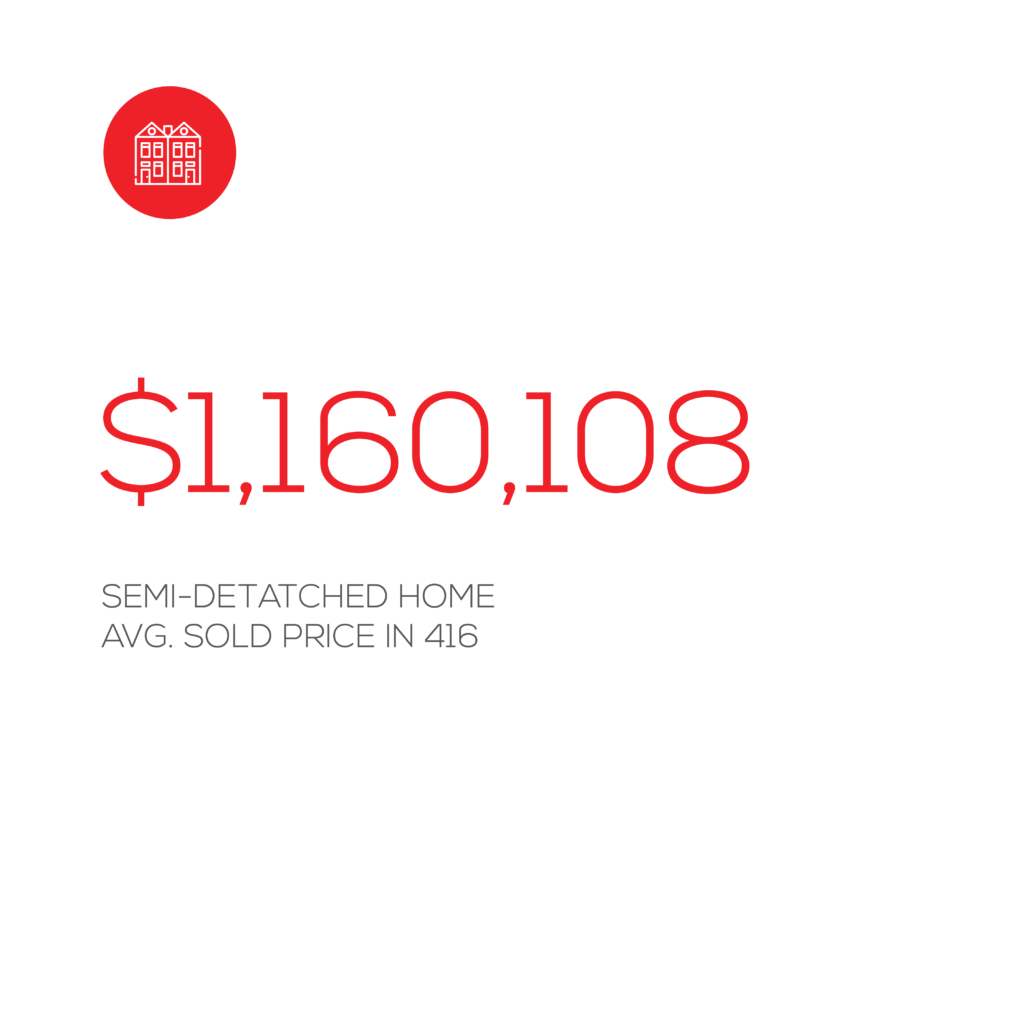

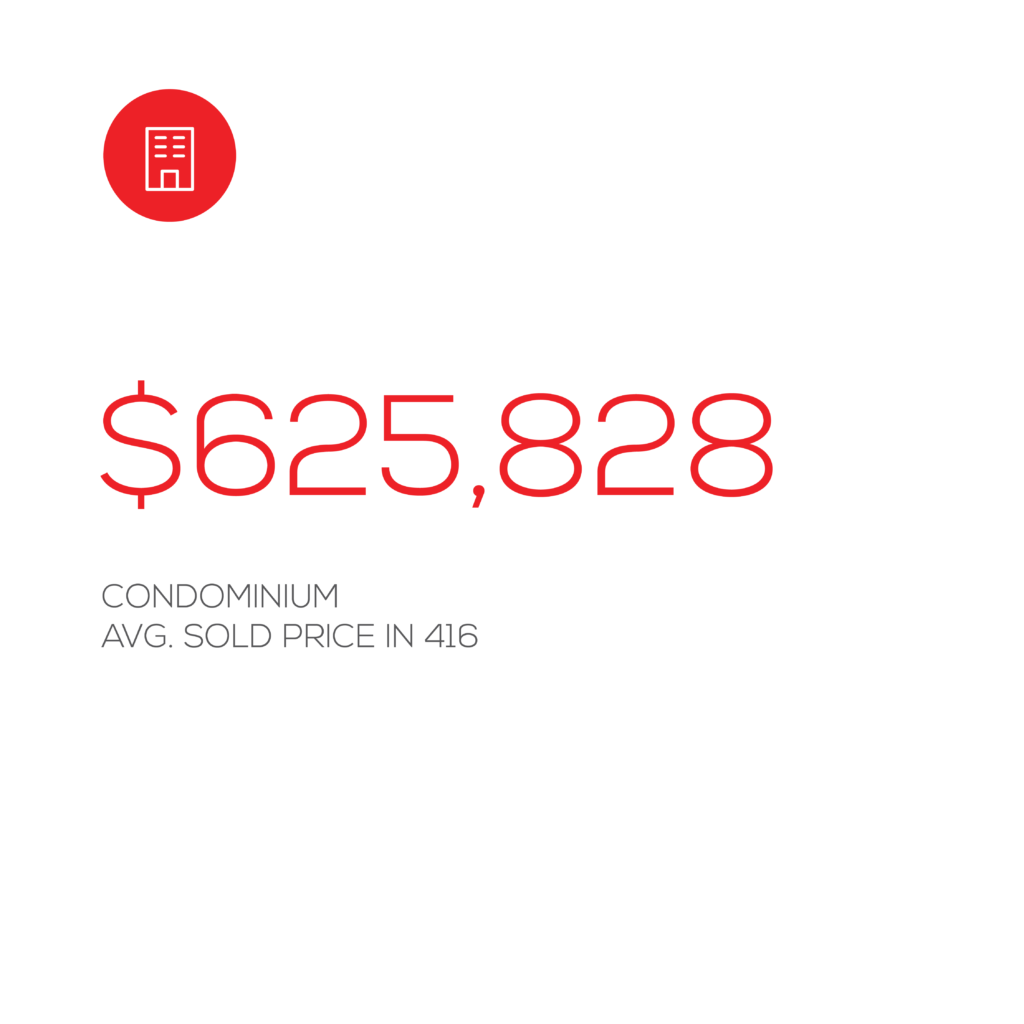

The aggregate price of a home in the Greater Toronto Area increased 17.3 per cent year-over-year, to $1,119,800, in the fourth quarter of 2021. Determined by housing type, the median price of a single-family detached home increased 22.4 per cent, to $1,421,200, while the median price of a condominium increased 14.8 per cent, to $665,400, during the same period.

“If the fourth quarter of 2021 is any indication of what is in store for the GTA housing market in the coming months, buyers can expect tight competition through the spring, as demand continues to outpace supply across the region and in every segment of the market,” said Karen Yolevski, chief operating officer at Royal LePage Real Estate Services Ltd. “This competition will continue to put upward pressure on prices, pushing some buyers to increase their budgets, expand the parameters of their geographical search or consider a different housing type.”

In the city of Toronto, the aggregate price of a home increased 8.1 per cent year-over-year, to $1,138,000, in the fourth quarter of 2021. During the same period, the median price of a single-family detached home increased 12.5 per cent, to $1,580,500, while the median price of a condominium increased 13.8 per cent, to $711,200.

“As affordability continues to wane in the downtown core and the greater region, demand for condominiums is increasing. Many first-time buyers, as well as those who have been priced out of the detached segment over the last year, see condos as an opportunity to enter the real estate market. Without a significant and speedy boost in housing supply, major urban centres like Toronto will remain firmly in a seller’s market.”

Yolevski noted that while many towns and smaller cities in the Golden Horseshoe have been affected by the trend of Torontonians migrating outside the city since the onset of the pandemic, most newcomers expected to enter Canada in 2022 will settle in one of the three largest urban centres. This will increase competition in both the re-sale and rental markets.

In December, Royal LePage issued a forecast projecting that the aggregate price of a home in the Greater Toronto Area will increase 11.0 per cent in the fourth quarter of 2022, compared to the same quarter in 2021.

“The shortage of homes available for sale or rent is one of the major social and economic challenges of our times,” said Phil Soper, president and CEO of Royal LePage. “Policy makers at all levels of government may take comfort from 2022’s very modest improvement in the supply of available properties relative to demand, yet we see home prices rising at double-digit levels again this year.”

Canada’s chronic housing shortage pre-existed the pandemic and with growing household formation and more newcomers to Canada adding to the demand, affordability is being threatened again.

“Everywhere, in our largest urban centres, and in the nation’s small and medium-sized towns and cities, new homes are not being built fast enough to satisfy growing demand,” said Soper. “In addition to the slow and expensive regulatory processes that burden builders, construction has been hampered by pandemic-specific challenges, including labour shortages and the increased cost of construction materials as suppliers struggle with supply chain issues. Some developers have been hesitant to commit to new projects.”

Canada’s inflation rate reached an 18-year high2 at the end of 2021, driven by increased costs to consumer goods, including gasoline and food, and significant delays in the supply chain. The Bank of Canada is expected to begin increasing its overnight lending rate incrementally later this year, which would result in higher mortgage rates.

While rising interest rates slow house price appreciation, higher borrowing costs will be coming off historical lows and the increases may not be enough to offset the significant upward price pressure from Canada’s housing supply crisis.

If you require more information on how this affects you directly, you can book a call or meeting by emailing info@reganteam.ca

December marked the end of a strong seller’s market year in the Greater Toronto Area, with demand consistently outstripping supply. We reached historic records in the GTA for the number of sold homes and average sold prices. A total of 121,712 sales were reported this year, the highest on record. We reached an all-time high average selling price of $1,095,475. In December, the number of transactions in the GTA was 6,031, a 15.7% decrease compared to the record of 7,154 set in December 2020. The average selling price was $1,157,849 in December 2021. This is a 24.2% year-over-year increase. New listings were down by 11.9% year-over-year.

Page 1 / 1

Zoom 100%

Can you imagine a day when you can put on a pair of glasses, anywhere in the world, and do a virtual walkthrough of a home? No, I’m not talking about a virtual tour. I’m talking about the ability to open cupboards. Take a look inside the fridge. Even check to see what type of lightbulb was used in a light fixture. All done through a virtual world. Not possible? Think again.

It’s called the Metaverse and it’s being dubbed as the next evolution of social connection. The Metaverse is a hypothesized iteration of the internet, supporting online 3-D virtual environments through conventional computers, as well as virtual and augmented reality headsets. Did you get all of that? Well, I’ll explain.

Companies like Facebook are investing copious amounts of money to make the world of shopping for things like clothing, shoes, and perhaps even housing a reality like no other. They’re on a mission to better establish a sense of presence for the consumer in a realistic environment that allows them to view and interact with and ultimately make a purchasing decision through what is essentially, a pair of glasses. As Mark Zuckerberg, CEO of Facebook puts it, “3D spaces in the metaverse will let you socialize, learn, collaborate and play in ways that go beyond what we can imagine.”

There is little doubt that Technology has given us the power to express ourselves and explore the world in greater ways than before. With the Metaverse, we won’t just be able to look at things or places, we’ll be able to experience it. We’ll be able to get together with friends, family, play, shop, to feel present no matter how far apart we actually are. Ultimately, we’ll be able to feel like we are literally, right there, in the moment. Instead of just viewing, say a photo or video of kids or grandkids, you’ll feel like you’re actually there, in that moment of time. Not just on your computer by yourself. You’ll be able to make eye contact and have a feeling of shared space. That deep feeling of presence.

In a recent article by the National Post it said that It’s no coincidence that this concept has sci-fi vibes to it, the term “metaverse” was originally coined in science fiction writer Neal Stephenson’s book “Snow Crash” in 1992 to describe a virtual world that people would plug into using their own virtual avatars. Online games like Second Life, which launched in 2003, were pioneers for metaverse economies, allowing users to trade goods and services using their in-game Linden dollars — including virtual real estate.

Some developers such as Microsoft have proposed using metaverse technology for improvements in work productivity. Instead of looking at someone on screen in a group setting such as Zoom, imagine a room full of people where one can make eye contact. Within the education sector, metaverse technologies have been proposed as a way to allow for interactive environments for learning. The metaverse could also host virtual reality home tours in the real estate sector.

Linden dollars may have been laughed at in the past but with the emergence of Cryptocurrencies being as real as dollar bills, who knows, maybe one day we’ll put on a headset and buy a home without ever stepping foot inside. I wonder if we’ll even live in a home 100 years from now? In the meantime, I like going into a home. Getting a sense for its character. Being able to see and touch. And of course, smell. I want to hear traffic patterns and the neighbourhood kids out on the street. But that’s just me.

For debate, a further discussion, or just a good old conversation, please feel to contact Matthew at Matthew@ReganTeam.Ca

Prestigious, desirable, and family-friendly are some terms that come to mind when anyone brings up Lorne Park real estate. And for good reason!

Keen to learn more about what this suburban residential neighbourhood has to offer? Read on to learn more.

With a prime location bordering the waterfront, north of Lake Ontario, it is no wonder Lorne Park had its beginnings as a recreational area for affluent Toronto vacationers in the early 1900’s.

With the launch of the QEW expressway that made the area all the more accessible, Lorne Park quickly blossomed into the exclusive enclave for the modern affluent community.

Part of the South Mississauga catchment with neighbouring Mineola, Clarkson, Lakeview, Port Credit districts, there is much to explore in the vicinity.

From schools, recreation to entertainment, Lorne Park has got you covered with everything you could possibly need within a quick drive!

If you are looking for a good school for your child, then Lorne Park is a fantastic option for you. Popularly known as the best school zone in Mississauga, Lorne Park has elementary, middle, and high schools which consistently rank in the top 10 or even top the city rankings.

Here are some amazing school choices in the Lorne Park district:

For those with little ones, there are even some great early education school options:

Hoping to spend quality time with the family? There are plenty of family-friendly recreational spaces around the neighbourhood that can keep them entertained. From waterfront parks, playgrounds, beaches, outdoor swimming clubs, nature trails, historical museums, libraries, and more, there is something for everyone.

Need some entertainment or dining options for the adults? All it takes is a quick trip to neighbouring Lakeshore and Port Credit – where bars and dining options are aplenty. A small price to pay for the quiet tranquillity you get in Lorne Park.

However, that is not to say there are not any essentials nearby. On the contrary, for their simple everyday needs, Lorne Park residents have a wealth of amenities in their vicinity:

While most homes in Lorne Park are typical detached suburban lots with sprawling front lawns and roomy garages, they come in all types of styles – from the traditional bungalows from its 60s-70s heydays to modern builds.

All of it comes with a relatively hefty price tag (popular lots can go up north of a million), as Lorne Park offers the allure of seclusion and tranquillity amidst a bustling waterfront catchment area.

Do you want the best schools for your kids and a peaceful environment with lots of outdoor and waterfront activities they can enjoy an active childhood? Do you enjoy winding down to the tranquillity of a quiet and safe neighbourhood? Do you appreciate living in a strong community of active and like-minded peers?

In short, are you looking for the perfect neighbourhood to raise your family?

Keen on finding out which Lorne Park Mississauga houses are for sale? Our team at The Regan Team will be more than happy to help you with navigating your home buying goals and dreams, every step of the way.

Simply drop us a message to kickstart your journey to finding your dream home today!

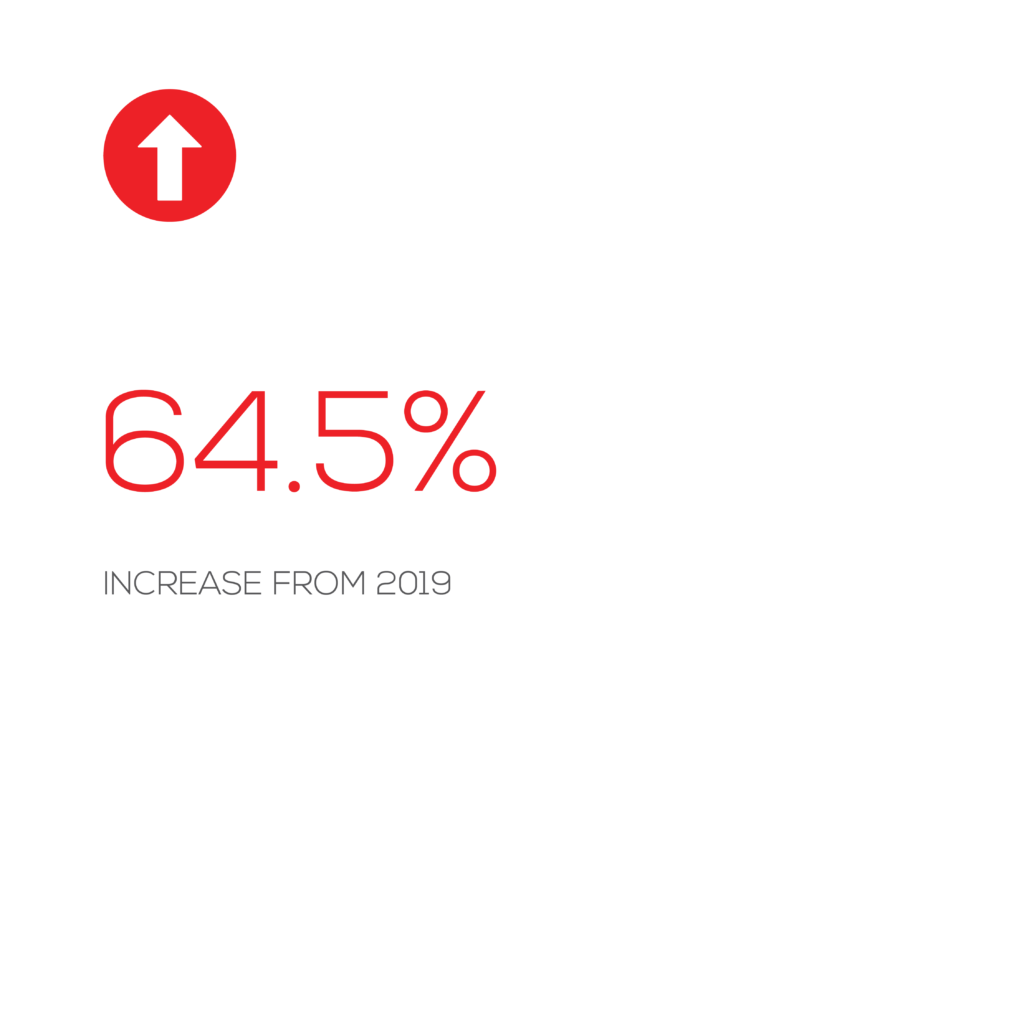

With over 95,000 home sales, the GTA real estate market had its third strongest year on record in 2020. This represents an 8.4% increase over 2019 results despite coming to a near-standstill last spring. December 2020 sales were up a remarkable 65% from a year ago. Overall prices accelerated further, particularly in the detached home sector, under extremely tight demand-supply conditions. Condo inventories swelled in December with active listings up 172% in the 416 and 159% in the GTA.

❄But while condo prices have continued to soften as inventories increase, their December 2020 sales were spectacular. At nearly 76% greater than for the same period last year, sales numbers indicate there’s no shortage of condo buyers in the GTA. Condos will be the market segment to watch in 2021.

Source: TREB statistics December 2020.